Interest rates have become a focal point for investors in the lead-up to the Federal Reserve’s two-day meeting earlier this week. Fed Chair Jerome Powell announced on Wednesday that the Fed will cut the federal funds rate by 0.50%, which marks the first rate reduction since 2020. Interest rates serve as a primary financial building block of the economy, which is why so much focus and attention has been placed on the Federal Reserve’s interest rate policy over the past several months.

Interest rates carry a lot of economic weight and have a significant impact on both the real economy and investment markets. Warren Buffett articulated this point well when he said that “interest rates are to asset prices like gravity is to the apple. They power everything in the economic universe.” Investors should consider rate impacts on investment holdings, markets, and the overall economy, however, consideration should also be given to the impact a changing rate environment has on long-range financial planning considerations.

Interest Rate Changes

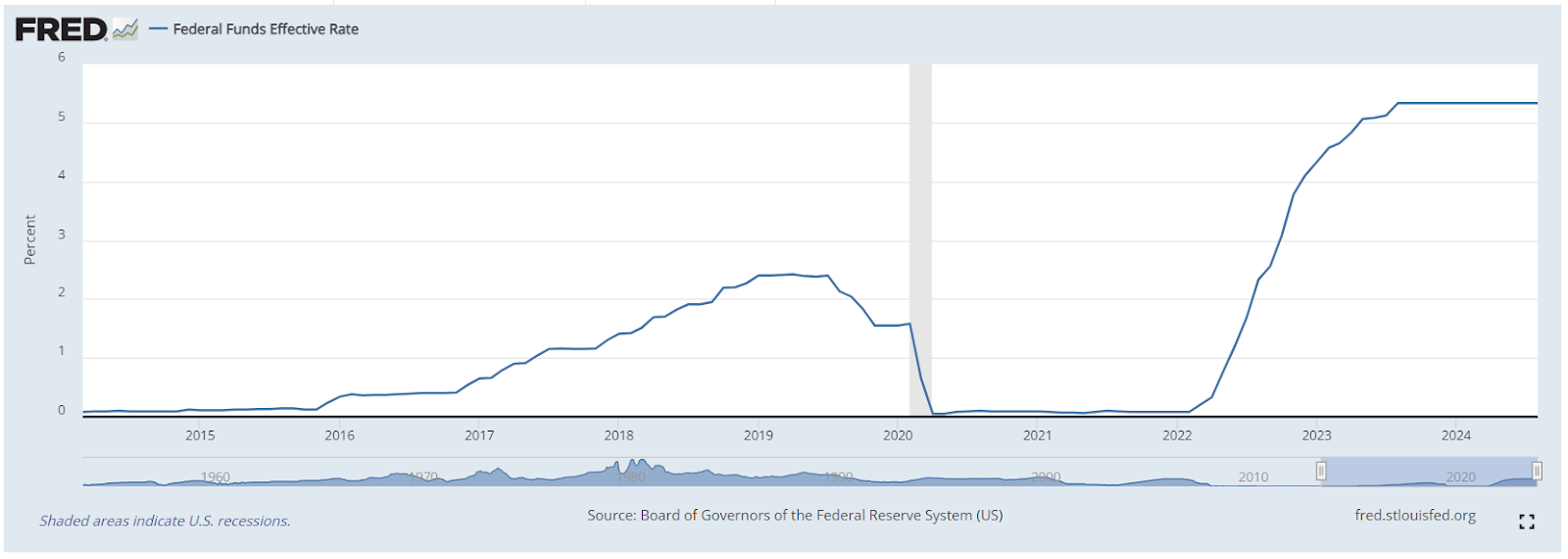

We are currently at a pivotal moment for interest rate policy. During the pandemic, severe economic restrictions were imposed as part of the solution to address the health crisis. In response, the Fed cut interest rates swiftly in 2020 in order to ease financial conditions. In addition, Congress paired this monetary policy response with several rounds of historic fiscal stimulus. This combination of fiscal and monetary support ultimately led to a surge in demand which outstripped supply. This imbalance produced high levels of inflation, which eventually peaked at 9.1% in June 2022.

To bring supply and demand back into balance and to get inflation under control, the Fed reversed course and began raising interest rates in March of 2022. Over the ensuing 16 months, the Fed raised rates 11 times from a range of 0.25% - 0.50% all the way to 5.25% - 5.50%, which is where we stood before this week’s Fed policy decision. This sharp increase in rates over a short period of time had a significant impact across the U.S. economy and investment markets. Both stock and bond markets posted negative returns for 2022, a historically rare event.

Inflation is not all the way back to the Fed’s 2% target, but the August consumer price index reading of 2.5% indicates that much progress has been made. The progress on inflation paved the way for the Fed to ease monetary conditions to support the economy and the labor market. Although the labor market is still in solid shape, softer data in recent months provided the catalyst needed for the Fed to cut rates.

Now that a shift in interest rate policy is underway, families should consider the financial implications. A change in Buffett's “economic gravity” will have far reaching impacts, and it’s a good time to reflect and consider planning updates.

Planning Considerations

Interest rates have an outsized impact on a number of estate planning strategies. The IRS publishes a series of interest rates used in estate planning calculations, and these rates are a big factor to consider when evaluating the relative benefit of one strategy over another. One example of an estate planning strategy impacted by rates is a Charitable Lead Trust (CLT), which is the type of trust former First Lady Jackie Kennedy Onassis included as a part of her estate plan, although it was not mandatory and ultimately not used by her heirs.

CLTs can be funded during life or after death and are linked to the IRS prescribed interest rate at the time of funding. Once funded, the CLT makes an annual payment to the named charity for the term of the trust, and thereafter transfers remaining trust assets to (non-charitable) beneficiaries. There are various types of CLTs with different features, but the strategy can be used to generate immediate tax deductions or to minimize estate taxes. The CLT works most effectively when the investment return on trust assets exceeds the IRS designated rate, which makes low interest rate environments ideal.

Pension calculations can also be heavily influenced by changing interest rates. Pension plans commonly give participants a choice at retirement between accepting an immediate lump sum or a lifetime payout. Although calculations vary from plan to plan, interest rates typically play a key role. When interest rates decrease, the present value of future payments increases, which leads to a higher lump sum payment. Lower rate environments favor lump sum payouts while higher rate environments favor lifetime payouts. For those nearing retirement with pension benefits, it’s very important to understand how your plan works and what impact interest rates have on payout options in order to maximize your benefits.

Whole life insurance policy dividends or crediting rates are yet another aspect of finances impacted by interest rates. Life insurance companies maintain their own investment portfolios and a portion of these assets are invested in fixed income securities. A sustained period of lower rates impacts fixed income returns, and reduced yields can, in turn, put pressure on insurance carriers to reduce dividend payouts to policyholders. It’s advisable to regularly monitor insurance policy performance to make sure it is in line with original projections. If actual rates are different than original expectations, dividends could be impacted and policy adjustments may be necessary.

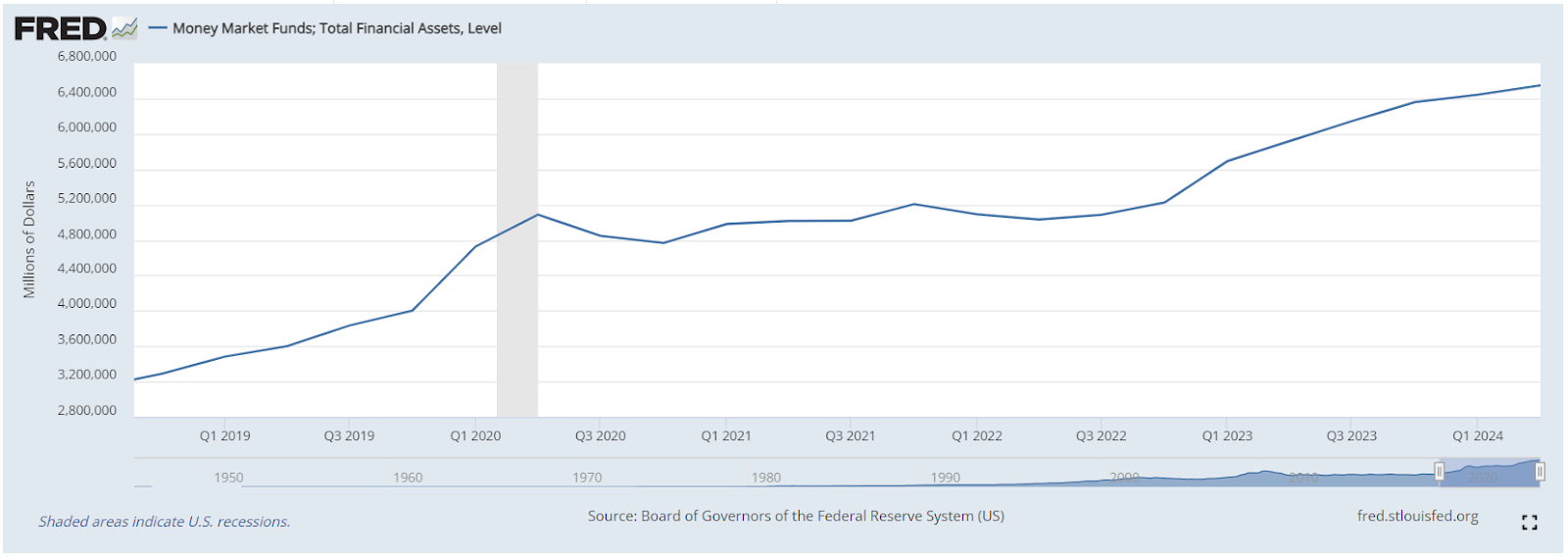

There are also key planning considerations with immediate ramifications, including impacts to cash yields. At the end of the second quarter, money market fund assets topped $6.5 trillion, marking a meaningful rise over the $4 trillion held at the end of 2019. Now that the Fed has cut the federal funds rate, money market rates will soon follow. Savers have enjoyed 5% cash yields for the past year but are now faced with the decision about how much cash to hold as rates decline. Adding nuance to allocation considerations is the current market backdrop in which bond yields have already started to decline, and the fact that the S&P 500 is relatively expensive compared with its long-term historical average.

We’re Here to Help

Falling interest rates will have a far-reaching impact on many financial planning decisions. As the U.S. pivots from one interest rate regime to another, we invite you to please reach out to us to help review the impacts of changing rates on your own long term goals and objectives.